Building a Real-Time Nigerian Stock Market Data Pipeline.

Building a Real-Time Nigerian Stock Market Analytics Pipeline: A data engineering and analytics project.

Introduction

The Nigerian Exchange (NGX) processes millions of naira in trades daily across various sectors, from banking giants such as GTCO Holdings to industrial powerhouses like Dangote Cement. But getting actionable insights from this market data requires more than just watching ticker symbols scroll by. It demands a robust data pipeline that can extract, transform, and visualize market movements to reveal opportunities.

In this post, I’ll walk you through how I built an end-to-end analytics platform for NGX equities data using Apache Airflow, PostgreSQL, and Tableau, one of the most used modern BI tools. Whether you’re a data engineer looking to build similar pipelines or an investor seeking to better understand market analytics, this project showcases practical patterns for real-time financial data processing.

The Challenge: Making Sense of Market Data

The Nigerian stock market data is publicly available through the NGX API, but raw data alone doesn’t answer the questions traders and analysts need:

Which stocks are gapping up or down at market open? (Price gaps often signal significant news or momentum)

How are different sectors performing? (Banking vs. Industrial Goods vs. Consumer Goods)

Who are the volume leaders? (High volume often precedes major price moves)

What’s the overall market breadth? (Are more stocks advancing or declining?)

To answer these questions at scale, I needed a system that could:

Fetch fresh data daily from the NGX API.

Store it reliably in a database.

Pre-compute complex analytics.

Serve insights through interactive dashboards.

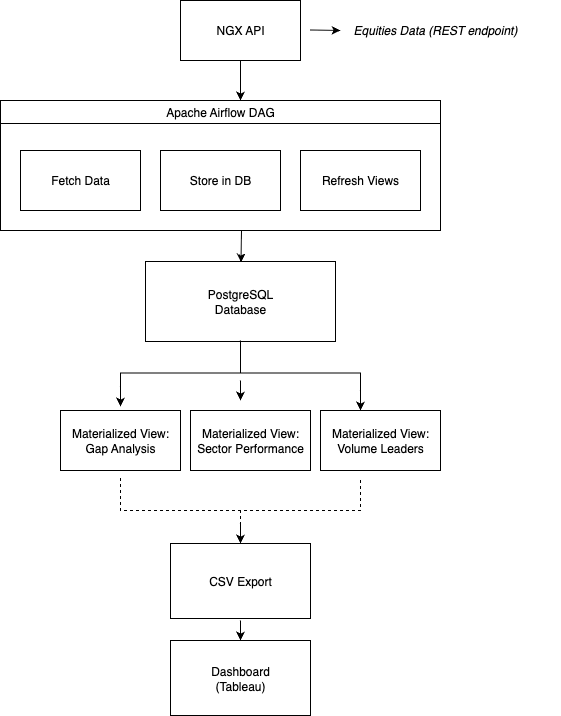

Overview of Architecture

Implementation Deep Dive

Data Extraction with Apache Airflow

The pipeline starts with an Airflow DAG that runs daily at 3 PM WAT—30 minutes after the Nigerian market closes at 2:30 PM. This timing ensures we capture all the data from the trading day.

import requests

import pandas as pd

def fetch_ngx_equities(**kwargs):

base_url = “https://doclib.ngxgroup.com/REST/api/statistics/equities/”

all_data = []

page = 0

page_size = 300

while True:

url = f”{base_url}?market=§or=&orderby=&pageSize={page_size}&pageNo={page}”

print(f”Fetching page {page}”)

response = requests.get(url, timeout=15)

response.raise_for_status()

data = response.json()

# Handle if the response is a list or a dict

if isinstance(data, list):

items = data

elif isinstance(data, dict):

items = data.get(”data”, [])

else:

print(f”Unexpected data type: {type(data)}”)

break

if not items:

print(”No more data — done”)

break

all_data.extend(items)

page += 1

df = pd.DataFrame(all_data)

The function fetch_ngx_equities.py uses Python’s requests library to download the NGX daily equities data from the API endpoint. The function returns a DataFrame with all the raw equity records. The API returns paginated data with 300 records per page, so we loop through all pages to capture the full market (typically 150-200 listed equities). Key data points include:

Symbol (e.g., DANGCEM, GTCO, MTNN)

Opening, High, Low, Closing prices

Volume and Value traded

Percentage change

Sector classification

Data Transformation

The API endpoint returns all the fields required for the analytics; however, there is still a need to ensure data consistency and quality. Tasks done in this step included:

Converting String data types to numeric columns

Filling missing values with zeros

df.columns = [col.lower() for col in df.columns] for col in [”prevclosingprice”,”openingprice”,”highprice”,”lowprice”,”closeprice”,”change”,”percchange”,”volume”, “value”]: if col in df.columns: df[col] = pd.to_numeric(df[col], errors=”coerce”).fillna(0)

Data Loading

The project uses a PostgreSQL database to store and retrieve data. The SQL script below creates an ngx_equities table in Postgres to store and update the daily datasets we retrieve.

CREATE TABLE IF NOT EXISTS ngx_equities (

id SERIAL PRIMARY KEY,

symbol VARCHAR(20),

company_name VARCHAR(100),

prev_closing_price NUMERIC,

opening_price NUMERIC,

high_price NUMERIC,

low_price NUMERIC,

close_price NUMERIC,

change NUMERIC,

per_change NUMERIC,

trades NUMERIC,

volume BIGINT,

market_value BIGINT,

sector VARCHAR(100),

date DATE

);The Airflow task truncates and reloads the table daily, ensuring clean, consistent data for analysis. For production systems that perform historical analysis, I’d recommend an append-only approach with date-based partitioning.

The Python function load_to_postgres.py was written to perform this task, and the script is shown in the code block below:

import pandas as pd

from airflow.providers.postgres.hooks.postgres import PostgresHook

def load_to_postgres(**kwargs):

ti = kwargs[’ti’]

file_path = ti.xcom_pull(task_ids=’fetch_ngx_equities’)

df = pd.read_csv(file_path)

pg_hook = PostgresHook(postgres_conn_id=’postgres_stock’)

pg_hook.run(”TRUNCATE TABLE ngx_equities;”)

conn = pg_hook.get_conn()

cursor = conn.cursor()

for _, row in df.iterrows():

cursor.execute(”“”

INSERT INTO ngx_equities (symbol, company_name, prev_closing_price, opening_price, high_price, low_price, close_price, change, per_change, trades, volume, market_value, sector, date)

VALUES (%s, %s, %s, %s, %s, %s, %s, %s, %s, %s, %s, %s, %s, CURRENT_DATE)

“”“, (

row.get(’symbol’),

row.get(’company2’),

row.get(’prevclosingprice’, 0),

row.get(’openingprice’, 0),

row.get(’highprice’, 0),

row.get(’lowprice’, 0),

row.get(’closeprice’, 0),

row.get(’change’, 0),

row.get(’percchange’, 0),

row.get(’trades’, 0),

row.get(’volume’, 0),

row.get(’value’, 0),

row.get(’sector’)

))

conn.commit()

cursor.close()

conn.close()The Concept of Materialized Views

Running complex analytical queries every time a user opens a dashboard would be slow and resource-intensive. PostgreSQL provides us with materialized views to solve this by pre-computing and storing query results as physical tables.

Unlike regular views that re-execute queries on every access, materialized views cache results and can be indexed for instant retrieval, which can be refreshed with a single command. They bridge the gap between real-time accuracy and performance, letting us decide when to update data rather than recalculating on every request.

For data pipelines and analytics workloads like our NGX equities dashboard, they enable instant access to various aggregated metrics without hitting the database with repetitive, expensive queries.

In view of this, we will be creating the following materialized views for our project

1. Daily Market Summary

CREATE MATERIALIZED VIEW mv_daily_market_summary AS

SELECT

CURRENT_DATE as trade_date,

COUNT(*) as total_stocks,

COUNT(CASE WHEN per_change > 0 THEN 1 END) as gainers,

COUNT(CASE WHEN per_change < 0 THEN 1 END) as losers,

COUNT(CASE WHEN per_change = 0 THEN 1 END) as unchanged,

SUM(volume) as total_volume,

SUM(market_value) as total_market_value,

SUM(trades) as total_trades,

AVG(per_change) as avg_percent_change

FROM ngx_equities;

2. Volume Leaders

CREATE MATERIALIZED VIEW mv_volume_leaders AS

SELECT

symbol,

company_name,

sector,

volume,

market_value,

trades,

per_change,

close_price,

ROW_NUMBER() OVER (ORDER BY volume DESC) as rank

FROM ngx_equities

WHERE volume > 0

ORDER BY volume DESC

LIMIT 10;

3. Value Leaders (Market Value)

CREATE MATERIALIZED VIEW mv_value_leaders AS

SELECT

symbol,

company_name,

sector,

market_value,

volume,

trades,

per_change,

close_price,

ROW_NUMBER() OVER (ORDER BY market_value DESC) as rank

FROM ngx_equities

WHERE market_value > 0

ORDER BY market_value DESC

LIMIT 10;

4. Most Active by Number of Trades

CREATE MATERIALIZED VIEW mv_most_active_trades AS

SELECT

symbol,

company_name,

sector,

trades,

volume,

market_value,

per_change,

close_price,

ROW_NUMBER() OVER (ORDER BY trades DESC) as rank

FROM ngx_equities

WHERE trades > 0

ORDER BY trades DESC

LIMIT 10;

5. Sector Performance

CREATE MATERIALIZED VIEW mv_sector_performance AS

SELECT

sector,

COUNT(*) as stock_count,

SUM(volume) as sector_volume,

SUM(market_value) as sector_market_value,

AVG(per_change) as avg_change,

COUNT(CASE WHEN per_change > 0 THEN 1 END) as sector_gainers,

COUNT(CASE WHEN per_change < 0 THEN 1 END) as sector_losers,

MAX(per_change) as best_performer,

MIN(per_change) as worst_performer

FROM ngx_equities

GROUP BY sector

ORDER BY sector_market_value DESC;

6. Price Volatility Leaders

CREATE MATERIALIZED VIEW mv_volatility_leaders AS

SELECT

symbol,

company_name,

sector,

opening_price,

high_price,

low_price,

close_price,

per_change,

volume,

-- Daily price range as percentage of opening price

CASE

WHEN opening_price > 0 THEN

((high_price - low_price) / opening_price) * 100

ELSE 0

END as volatility_percent,

trades

FROM ngx_equities

WHERE opening_price > 0

AND high_price > 0

AND low_price > 0

ORDER BY volatility_percent DESC

LIMIT 20;

7. Gap Analysis (Opening vs Previous Close)

CREATE MATERIALIZED VIEW mv_gap_analysis AS

SELECT

symbol,

company_name,

sector,

prev_closing_price,

opening_price,

close_price,

per_change,

volume,

market_value,

-- Gap percentage

CASE

WHEN prev_closing_price > 0

THEN ((opening_price - prev_closing_price) / prev_closing_price) * 100

ELSE 0

END as gap_percent,

-- Gap type

CASE

WHEN opening_price > prev_closing_price THEN ‘Gap Up’

WHEN opening_price < prev_closing_price THEN ‘Gap Down’

ELSE ‘No Gap’

END as gap_type

FROM ngx_equities

WHERE prev_closing_price > 0

AND opening_price > 0

AND ABS(opening_price - prev_closing_price) / prev_closing_price > 0.01

ORDER BY ABS((opening_price - prev_closing_price) / prev_closing_price) DESC

LIMIT 20;

8. Low Liquidity Warning

CREATE MATERIALIZED VIEW mv_low_liquidity AS

SELECT

symbol,

company_name,

sector,

close_price,

volume,

market_value,

trades,

CASE

WHEN trades = 0 THEN ‘No Trading Activity’

WHEN trades <= 5 THEN ‘Very Low Activity’

WHEN volume < 1000 THEN ‘Low Volume’

ELSE ‘Low Liquidity’

END as liquidity_status

FROM ngx_equities

WHERE trades <= 10 OR volume < 5000

ORDER BY trades ASC, volume ASC;

9. Top Gainers

CREATE MATERIALIZED VIEW mv_top_gainers AS

SELECT

symbol,

company_name,

sector,

prev_closing_price,

close_price,

per_change,

volume,

market_value,

trades,

ROW_NUMBER() OVER (ORDER BY per_change DESC) as rank

FROM ngx_equities

WHERE per_change > 0

ORDER BY per_change DESC

LIMIT 10;

10. Top Losers

CREATE MATERIALIZED VIEW mv_top_losers AS

SELECT

symbol,

company_name,

sector,

prev_closing_price,

close_price,

per_change,

volume,

market_value,

trades,

ROW_NUMBER() OVER (ORDER BY per_change ASC) as rank

FROM ngx_equities

WHERE per_change < 0

ORDER BY per_change ASC

LIMIT 10;

11. Comprehensive Stock Overview

CREATE MATERIALIZED VIEW mv_stock_overview AS

SELECT

id,

symbol,

company_name,

sector,

prev_closing_price,

opening_price,

high_price,

low_price,

close_price,

change,

per_change,

trades,

volume,

market_value,

CASE

WHEN opening_price > 0 THEN

((high_price - low_price) / opening_price) * 100

ELSE 0

END as daily_volatility,

CASE

WHEN volume > 0 THEN market_value / volume

ELSE 0

END as avg_trade_price,

CASE

WHEN per_change > 0 THEN ‘Gainer’

WHEN per_change < 0 THEN ‘Loser’

ELSE ‘Unchanged’

END as performance_category,

CASE

WHEN trades >= 100 THEN ‘High Activity’

WHEN trades >= 20 THEN ‘Medium Activity’

WHEN trades > 0 THEN ‘Low Activity’

ELSE ‘No Activity’

END as activity_level

FROM ngx_equities

ORDER BY market_value DESC;

Materialized views automated refresh pipeline

The Materialized views we created need to be refreshed after each successful ETL run to reflect new data. The Airflow DAG handles this automatically via a Postgres operator:

from airflow.providers.postgres.hooks.postgres import PostgresHook

def refresh_materialized_views(**kwargs):

pg_hook = PostgresHook(postgres_conn_id=’postgres_stock’)

refresh_queries = [

“REFRESH MATERIALIZED VIEW mv_daily_market_summary;”,

“REFRESH MATERIALIZED VIEW mv_gap_analysis;”

“REFRESH MATERIALIZED VIEW mv_low_liquidity;”,

“REFRESH MATERIALIZED VIEW mv_momentum_stocks;”

“REFRESH MATERIALIZED VIEW mv_most_active_trades;”,

“REFRESH MATERIALIZED VIEW mv_sector_performance;”

“REFRESH MATERIALIZED VIEW mv_top_gainers;”,

“REFRESH MATERIALIZED VIEW mv_top_losers;”,

“REFRESH MATERIALIZED VIEW mv_value_leaders;”

“REFRESH MATERIALIZED VIEW mv_volatility_leaders;”,

“REFRESH MATERIALIZED VIEW mv_volume_leaders;”,

“REFRESH MATERIALIZED VIEW mv_stock_overview;”

]

conn = pg_hook.get_conn()

cursor = conn.cursor()

for query in refresh_queries:

cursor.execute(query)

print(f” Executed: {query}”)

conn.commit()

cursor.close()

conn.close()The complete DAG workflow executes in the sequence:

Fetch Data → Load to PostgreSQL → Refresh Materialized Views → Export to CSVEach task only runs if the previous one executes successfully, ensuring data integrity throughout the pipeline.

Exporting for Visualization

The visualization is done in Tableau, and since the intent is to share the dashboard publicly, I used the Tableau Public version, which requires CSV files. The pipeline was designed to automatically export all materialized views to CSV files.

def export_materialized_views_to_csv(**kwargs):

pg_hook = PostgresHook(postgres_conn_id=’postgres_stock’)

# Define all your materialized views to export

materialized_views = [

‘mv_daily_market_summary’,

‘mv_gap_analysis’,

‘mv_low_liquidity’,

‘mv_momentum_stocks’,

‘mv_most_active_trades’,

‘mv_sector_performance’,

‘mv_top_gainers’,

‘mv_top_losers’,

‘mv_value_leaders’,

‘mv_volatility_leaders’,

‘mv_volume_leaders’,

‘mv_stock_overview’,

]

# Output directory for Tableau CSVs

output_dir = “/opt/airflow/outputs/materialized_views_data”

os.makedirs(output_dir, exist_ok=True)

conn = pg_hook.get_conn()

exported_files = []

total_rows = 0

for view_name in materialized_views:

try:

print(f”Exporting {view_name}...”)

# Query the materialized view

query = f”SELECT * FROM {view_name};”

df = pd.read_sql_query(query, conn)

# Export to CSV

csv_path = f”{output_dir}/{view_name}.csv”

df.to_csv(csv_path, index=False)

row_count = len(df)

total_rows += row_count

exported_files.append(view_name)

print(f” {view_name} exported successfully ({row_count} rows) -> {csv_path}”)

except Exception as e:

print(f”✗ Error exporting {view_name}: {e}”)

conn.close()

return {

‘exported_files’: exported_files,

‘total_rows’: total_rows,

}This creates a fresh set of CSV files daily, which are connected and refreshed on Tableau Public for updated visualizations.

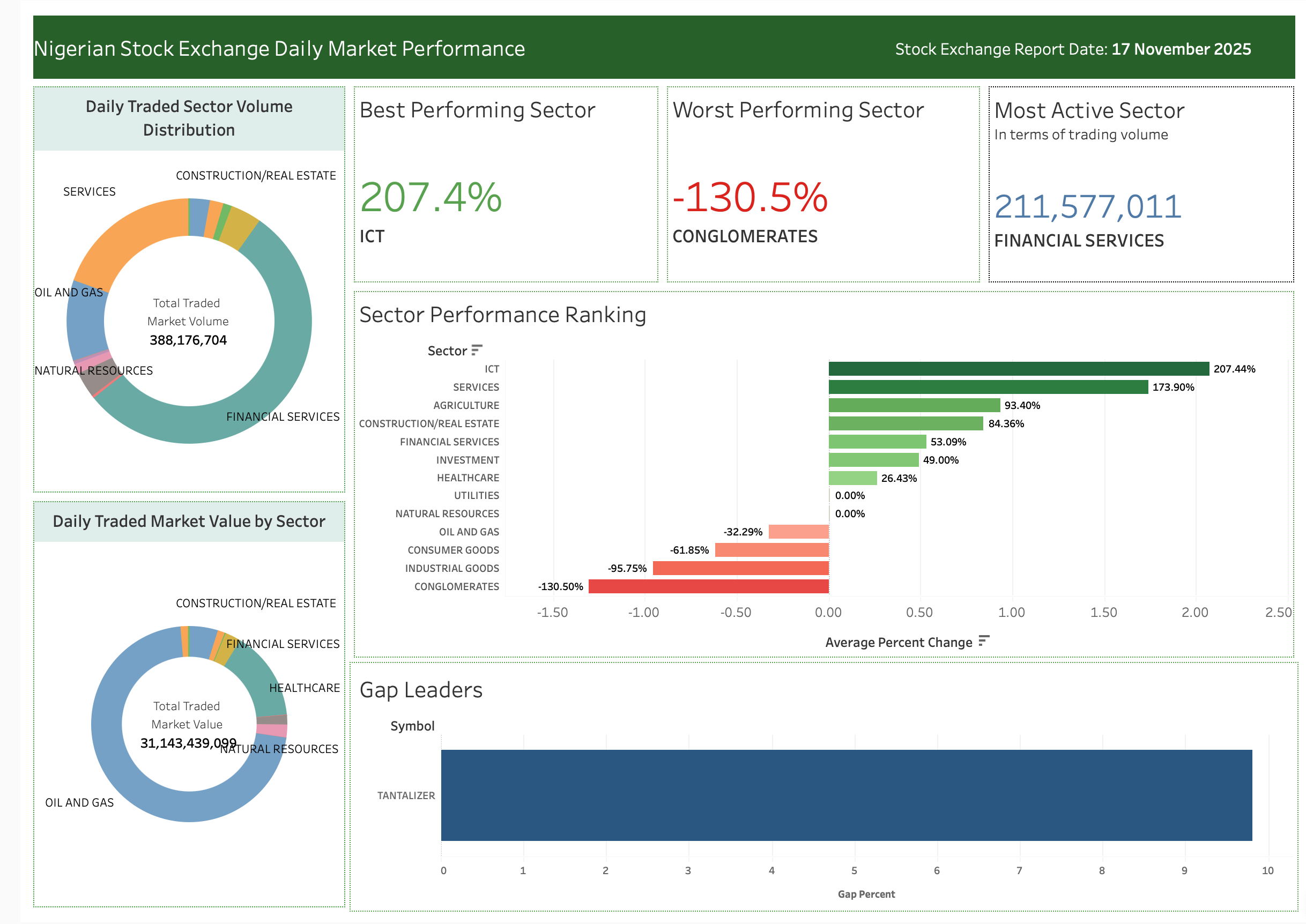

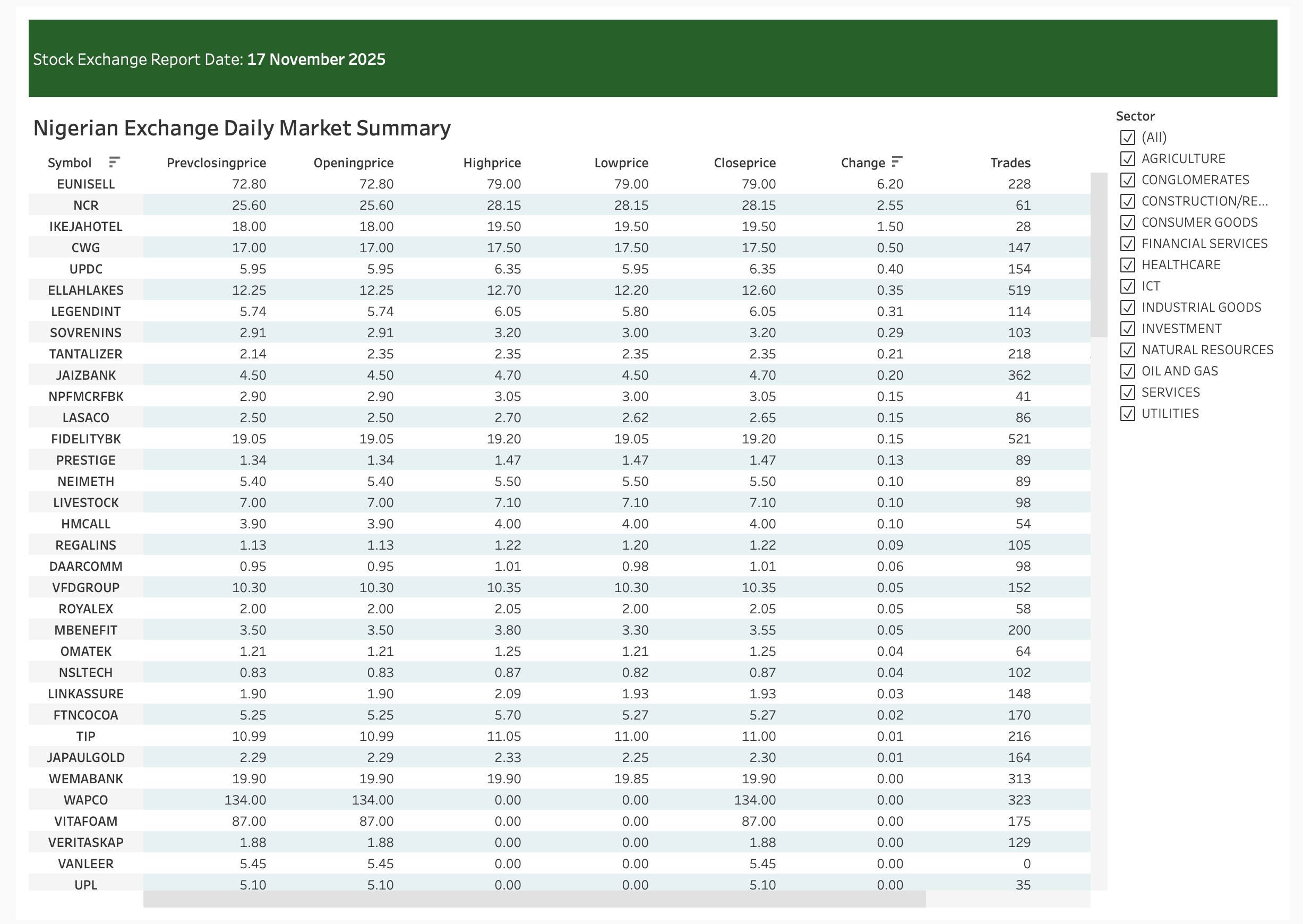

Dashboard Designs: Getting Insights from the Data

Click here to view the Nigerian stock market sector performance dashboard.

Click here to view the Nigerian stock market equity prices dashboard

The pipeline feeds multiple dashboards designed to answer specific questions:

Gap Analysis Dashboard

Purpose: Identify stocks with significant overnight price gaps

Business Value: Traders can quickly spot stocks that opened with unusual price movements, often indicating news events or institutional activity.

Sector Performance Dashboard

Purpose: Track relative sector strength and rotation

Business Value: Portfolio managers can identify sector rotation patterns and adjust allocations accordingly. For example, if Banking is underperforming while Industrial Goods rallies, it might signal a defensive rotation.

Top Gainers & Losers Dashboard

Purpose: Surface the day’s biggest movers

Business Value: Momentum traders can identify strong trends, while risk managers can spot unusual volatility in specific stocks.

Volume Leaders Dashboard

Purpose: Identify unusual trading activity

Business Value: High volume often precedes major price moves. Institutional accumulation or distribution typically shows up as above-average volume before the stock makes a significant move.

Market Overview Dashboard

Purpose: Comprehensive market health snapshot

Business Value: A holistic view of market sentiment. When breadth is strong (many more advancers than decliners), it indicates broad market strength rather than narrow leadership.

Technical Decisions & Trade-offs

Why Apache Airflow?

Built for data pipelines with dependency management

Excellent monitoring and alerting

Retry logic and error handling out of the box

Scales well (can distribute tasks across multiple workers)

Decision: Given the multi-step workflow with dependencies (fetch → store → refresh → export → validate), Airflow’s orchestration capabilities justify the setup overhead.

Why PostgreSQL?

Pros:

Excellent analytics performance with proper indexing

Materialized views are a first-class feature

ACID compliance ensures data integrity

Free and open-source

Cons:

Not optimized for extremely high-frequency updates (not an issue for daily batch processing)

Decision: Perfect fit for this use case. Daily batch updates, complex analytical queries, and materialized view support make PostgreSQL ideal.

Why Materialized Views Over Regular Tables?

I could have written Python/Pandas code to calculate these metrics and insert them into regular tables. Why materialized views?

Advantages:

Declarative SQL is easier to review and modify than procedural code

Automatic refresh with a single command (

REFRESH MATERIALIZED VIEW)Consistency - all views refresh from the same base table snapshot

Indexable - can add indexes for even faster queries

Less code to maintain - no Python logic for aggregations

Trade-offs:

Requires PostgreSQL (not portable to other databases without changes)

Refresh takes time (though

REFRESH MATERIALIZED VIEW CONCURRENTLYsolves this for production)

Future Enhancements

Historical Data Storage

Currently, the pipeline only keeps the latest day’s data. To enable trend analysis, I plan to:

Switch from

TRUNCATEtoINSERTwith date partitioningCreate time-series views showing week-over-week, month-over-month changes

Add moving averages and momentum indicators

Real-Time Updates

For intraday trading, daily updates aren’t enough. Enhancements could include:

Streaming data ingestion (Kafka + Flink)

Incremental materialized view refreshes

Machine Learning Integration

With historical data, we could build:

Anomaly detection (unusual volume or price moves)

Sector rotation predictions

Momentum scoring algorithms

Portfolio optimization models

Alerting & Notifications

Traders want to know immediately when:

A stock gaps up/down more than 5%

Volume exceeds 2x the average

A sector rotation occurs

I could add alerting via email or SMS.

Multi-Exchange Support

Expanding beyond NGX to include:

Other African exchanges (JSE, EGX, NSE Kenya)

Comparative analysis across markets

Currency normalization for cross-border comparisons

Conclusion

Building this NGX equities analytics pipeline taught me that great data engineering isn’t just about moving data—it’s about creating systems that deliver insights reliably and efficiently.

Key Takeaways:

Orchestration matters - Airflow turns a fragile script into a robust, monitored pipeline

Materialized views are powerful - Pre-computing queries can improve performance by orders of magnitude

Design for failure - APIs fail, networks timeout, data is messy. Handle it gracefully

Start simple, iterate - A working MVP beats a perfect plan that never ships

Visualization is the payoff - All the engineering enables one thing: better decisions

Whether you’re analyzing stock markets, e-commerce data, or IoT sensors, these patterns apply. Extract data reliably, transform it intelligently, store it efficiently, and visualize it effectively.

The complete code for this project is available on GitHub here

Let’s Connect

I’m always interested in discussing data engineering, financial analytics, and building robust pipelines. Whether you’re working on similar projects or have questions about this implementation:

If you found this useful, feel free to share it with your network. And if you’re building something similar, I’d love to hear about your approach and challenges!

All data is sourced from publicly available NGX APIs. This is for educational purposes and is not financial advice.

It's interesting how you picked this stack. Very robust pipeline. Curios about streaming options.